Investors who had sought shelter at YTL Hospitality REIT (YTL REIT) as the economic climate was getting unfavourable should have not many regrets over the past three years.

Not only is it the sole REIT listed on Bursa Malaysia that specifically invests in hotel and hospitality assets in the region, offering investors exposure to the regional tourism industry, but against a backdrop of oversupply of commercial properties such as shopping malls and office space, it is also a safe haven for investors who want steady yield.

YTL REIT announced attractive dividends for FY2018, paying a distribution per unit (DPU) of 7.8683 sen. This translates into a yield of 6.73%, based on the 12-month weighted average market price of RM1.17 per unit.

Moreover, the total distribution of RM134.1 million represents nearly 100% of its realised and distributable income for FY2018. This is in line with its policy to distribute at least 90% of distributable income for each financial year.

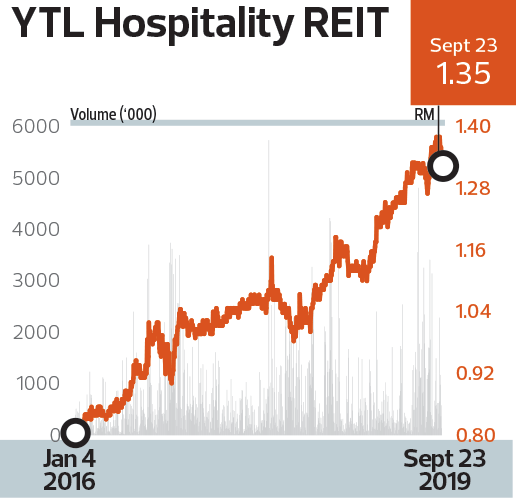

The REIT’s unit price has been growing firmly over the past three years, from 84 sen on March 31, 2016, to RM1.24 on March 29, 2019, which translates into a three-year compound average growth rate (CAGR) of 14%. More recently, the REIT closed at an all-time high of RM1.38 on Aug 30, 2019, giving the REIT a valuation of RM2.35 billion.

Mirroring its upward-trending unit price, the group’s net property income (NPI) rose from RM201.5 million in FY2015 to RM248.8 million in FY2018, indicating a three-year CAGR of 7.28%.

YTL REIT saw its profit after tax grow from RM95 million in FY2015 to RM236.6 million in FY2018, representing a three-year CAGR of 35.6%. Its FY2018 performance was stellar compared with its loss-making years previously — recording negative profits of RM12.1 million in FY2017 and RM5.8 million in FY2016.

Its revenue also grew in tandem with profits, from RM417.7 in FY2015 to RM501 million in FY2018, giving a three-year CAGR of 6.25%. The increases in revenue and NPI were mainly due to revenue contribution from the acquisition of The Majestic Hotel Kuala Lumpur.

As at June 30, 2018, the REIT’s investment portfolio stood at RM4.27 billion, of which 48% is derived from Malaysia, 45% from Australia, and the remainder 7% from Japan, according to its 2018 annual report. This is an 11.6% increase from FY2017’s RM3.91 billion.

YTL REIT bought over The Majestic Hotel Kuala Lumpur in FY2018. Other hospitality assets in the REIT’s investment portfolio in Malaysia are JW Marriott Hotel Kuala Lumpur, The Ritz-Carlton, Kuala Lumpur — Suite Wing, Cameron Highlands Resort, Vistana Penang Bukit Jambul, Vistana Kuala Lumpur Titiwangsa, Vistana Kuantan City Centre, The Ritz-Carlton, Kuala Lumpur — Hotel Wing, Tanjong Jara Resort and part of Pangkor Laut Resort.

The international assets in its investment portfolio are Hilton Niseko Village in Japan — which was recently acquired through the REIT’s subsidiary, Starhill REIT Niseko GK – as well as Sydney Harbour Marriott, Brisbane Marriott and Melbourne Marriott in Australia.

Maybank IB Research analyst Kevin Wong has maintained a “buy” call on the REIT based on its deep value, premised on the earnings upside from a recovery of its Australian hotels’ performance and from its rich pipeline of assets, as well as resilient earnings from its master-lease assets.

“YTL REIT offers a total return of 21% – including a favourable FY2020 net DPU yield of 6%,” he writes in a research note on Aug 1, adding that earnings would mainly be growing organically in the near term.

He said growth catalysts will be from the rich pipeline of hospitality assets from its sponsor, YTL Corp Bhd, mainly within Southeast Asia and Europe, which is backed by its gross gearing of 0.41 times (end-FY2019) based on debt headroom of about RM846 million.